Tiger Research: DeFi no longer pursues high interest rates, interest-stabilized currency is the new capital.

DeFi is moving from a market for production earnings to a market for traditional financial imports and distribution of revenues. The more stable the foundation, the stronger the upper structure. 。

The report was written by Tiger Research。DeFi is moving from a market for production earnings to a market for traditional financial imports and distribution of revenues. The more stable the foundation, the stronger the upper structure。

Core elements

- sUSDE halved supply while capital went to the lower-yield USYC and USDS. It's not a capital exit. It's a change in selection criteria

- APY IS NO LONGER A DIVIDING LINE FOR ASSETS. MORE IMPORTANT IS THE POSSIBILITY OF BEING ADOPTED AS COLLATERAL, SAVINGS OR RESERVES

- S& P gives the USDS the first credit rating in the history of the DeFi protocol, and gives USDe a 120% risk right Heavy

- Ethena will overhaul the collateral structure in April 2026 from synthetic to hybrid models. Single revenue sources are no longer sufficient to survive in YBS markets

- DeFi is moving from a market for production earnings to a market for traditional financial imports and distribution of revenues. The more stable the foundation, the stronger the upper structure

what happened behind the susde

THE INTEREST-BEARING STABILITY COIN (YBS) IS AN ANCHORED UNITED STATES DOLLAR AND HOLDS A LIVING CURRENCY. USDC AND USDT LIKE CASH, YBS LIKE DEPOSIT, VALUE UP WITH INTEREST RATES。

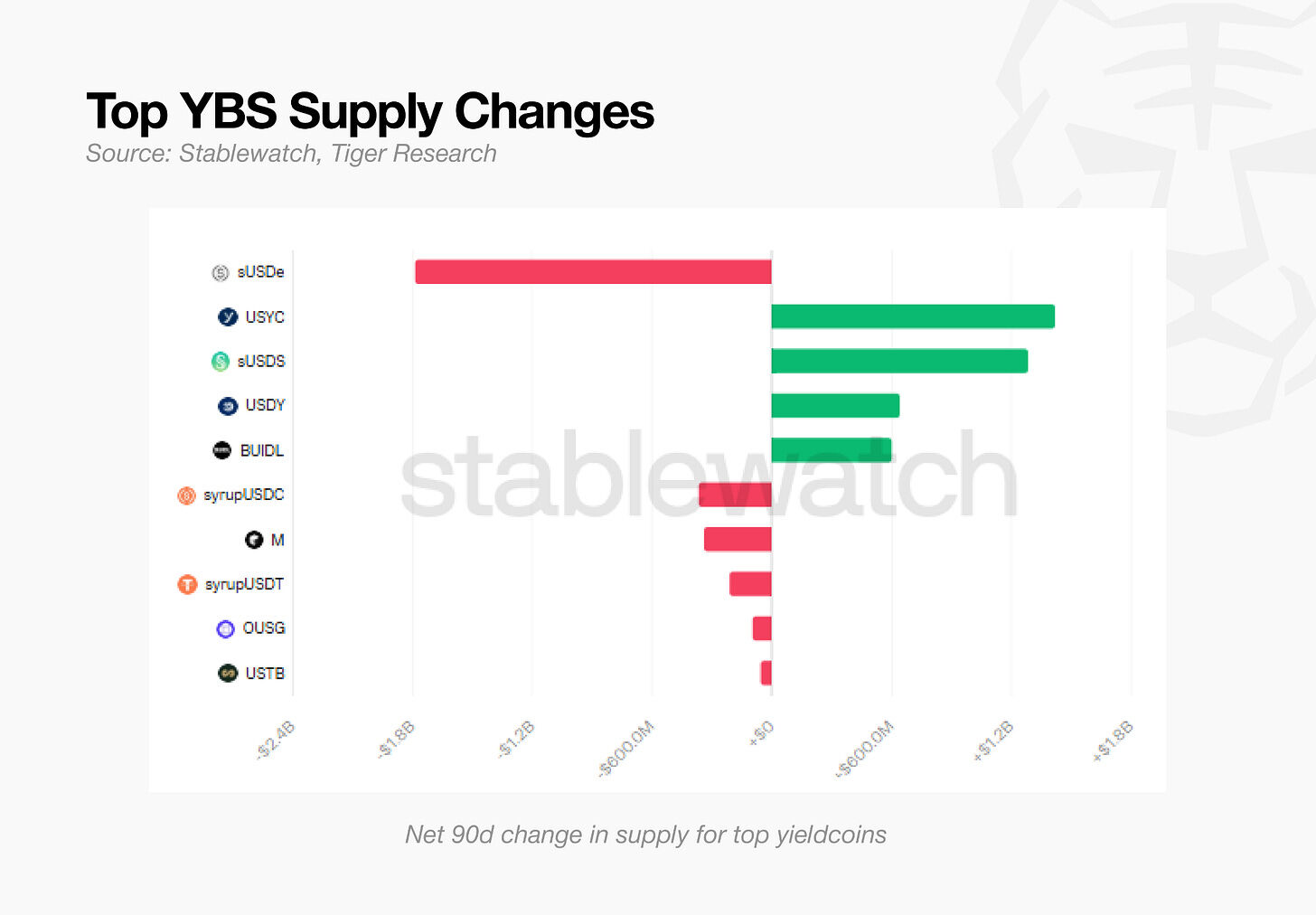

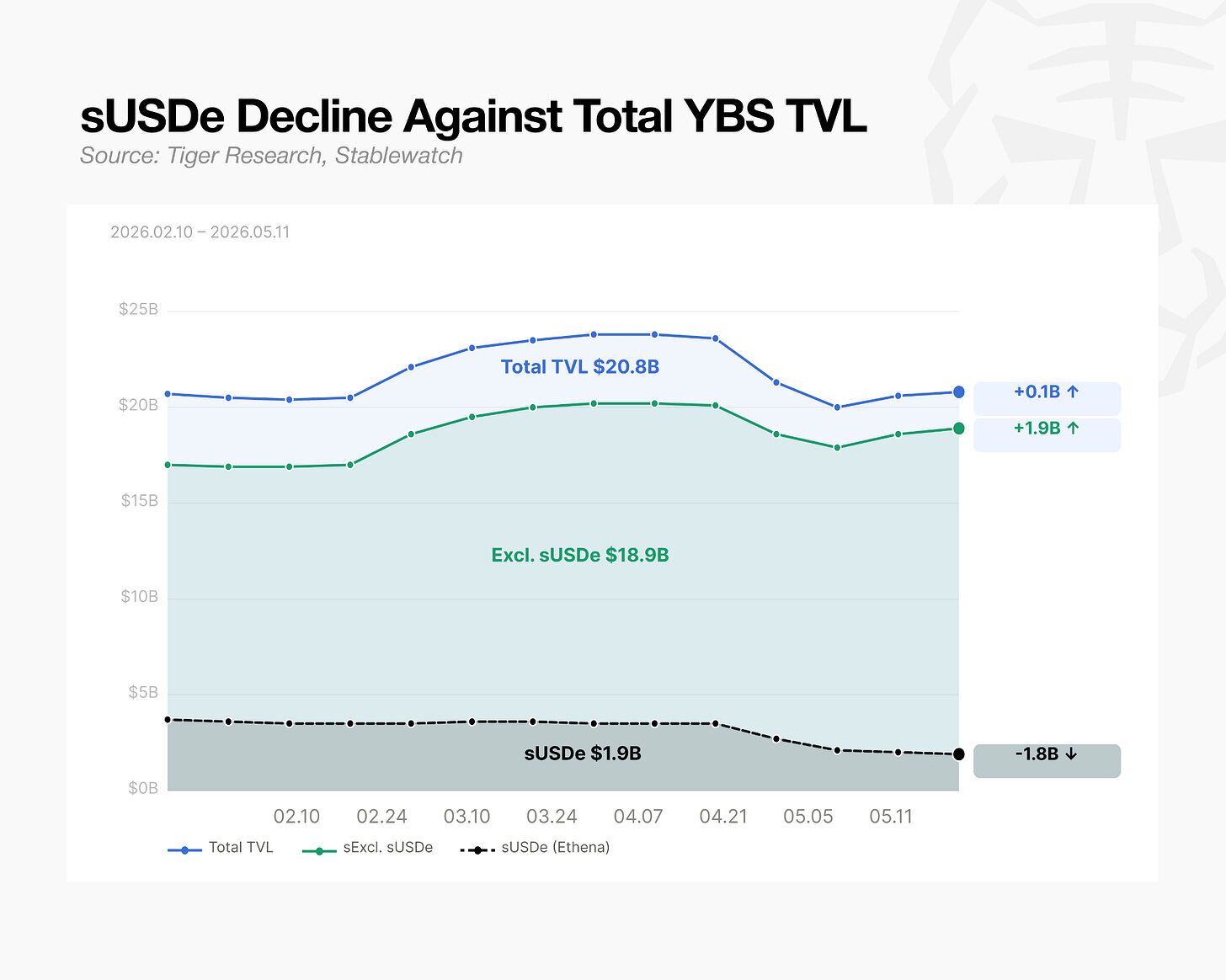

The market is undergoing unusual changes. Ethena's flagship product sUSDe used to own more than 30 per cent of the YBS market, and supply fell by about $1.8 billion over the past 90 days, down 49 per cent from its peak. No hacker attack, no protocol failure。

But the market itself did not shrink. During the same period, the total YBS TVL actually rose. Within 90 days, USYC (Circle ' s Treasury Support Stabilisation Currency) went to $1.4 billion and USDS (Sky ' s Mixed Stabilisation Currency) to $1.2 billion. These two inflows combined exceeded the fall of the sUSde。

If you look at the flow of funds, you can tell different stories. Capital does not depart, but rotates in the same market。

MORE IMPORTANT THAN ASY: HOLDER BASE AND BOTTOM ASSET

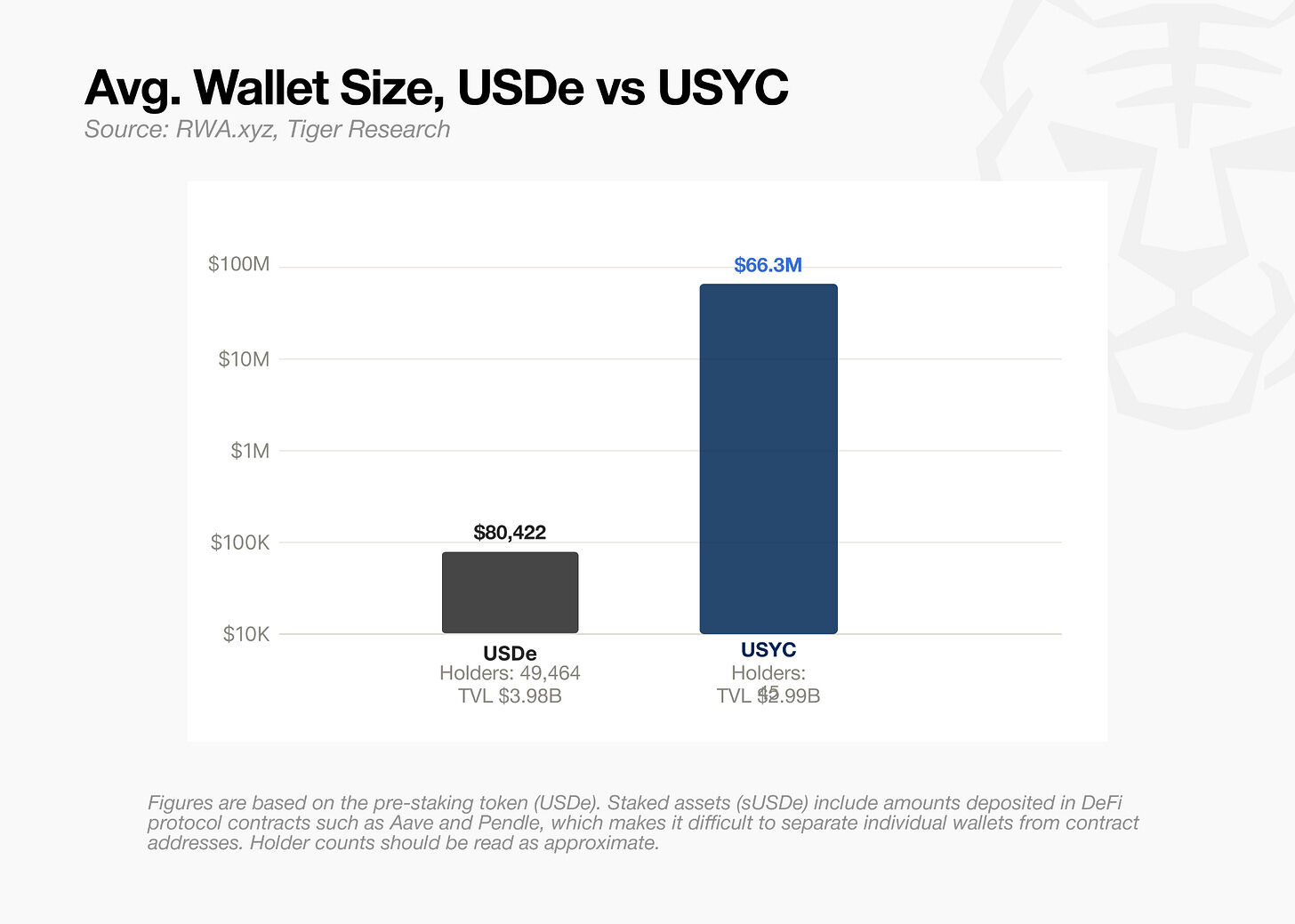

Look at APY alone, there's no reason to transfer the money. Under the 30-day benchmark, USYC is about 3 per cent, SUSDS is about 3.6 per cent, and SUSDE is actually higher, about 4 per cent. If the rate of return is the driving force, the funds should be concentrated in sUSde. The transfer does not appear to come from the proceeds, but from two other factors: (1) the holder base, and (2) the lower assets。

Batteries and institutions

Based on the average holdings per wallet, the USDE holder is approximately 1/800 for USYC holders. The gap has widened further with the elimination of large block purchases. The USYC was designed from the outset to attract only large amounts of money, and USDE is heavily dependent on the diaspora。

U.S.De and USYC split up on the hold。

For USDE, the investment arguments of the diaspora and institutional holders revolve around the rate of return. They're coming for ASY, and ASY goes off. The USYC takes different paths: it is not dispersed, with institutional applications at its core。

The USYC is open only to eligible investors, with a minimum purchase threshold of $100,000. In July 2025, it was adopted as an institutional derivative collateral. Once traders can mortgage assets on the largest exchange, demand follows. BNB Chain alone released $2.54 billion。

Delta neutral vs RWA

The difference between USDe and USDS comes from reserve assets. What agencies want is predictability — predictability in how the gains are generated and how they fluctuate。

USDe runs the delta neutral structure: on the one hand is encrypted collateral and on the other is the void of a lasting contract to offset price fluctuations. Gains are linked to the sustainable funding rate. In 2024, sUSDE ASY exceeded 47%. When the market turned across, it fell to 3 per cent. The fluctuations were more than ten times greater in a few months. Rates of return fluctuated simultaneously with market conditions。

USDS IS SUPPORTED BY THE SHORT-TERM UNITED STATES TREASURY AND MONETARY MARKET FUND. THE RATE OF RETURN IS LINKED TO REAL WORLD INTEREST RATES. AT THE END OF THE YEAR, IT TOOK MORE THAN A YEAR FOR ASY TO FALL TO 3% IN 9% OF THE DISTRICTS。

This difference is also reflected in the assessment of S& P. In August 2025, S& P Global gave Sky Protocol a B-credit rating, the first credit rating ever given to the DeFi agreement. The ratings themselves are low, and the important thing is that the DeFi agreement has a credit rating。

In the same report, USDe was marked as 1250% risk weight. The reason is "complex maintenance mechanisms". Under Basel III (Bank capital adequacy framework developed by BIS), USDE is classified as the highest risk encrypted asset category. Independent of any incident, sUSde is outside the scope of approval by the Agency Risk Committee。

Predictability and rates of return are equally important for institutions. Ethena can provide higher returns based on market conditions, but institutional trading platforms may be more difficult to cover。

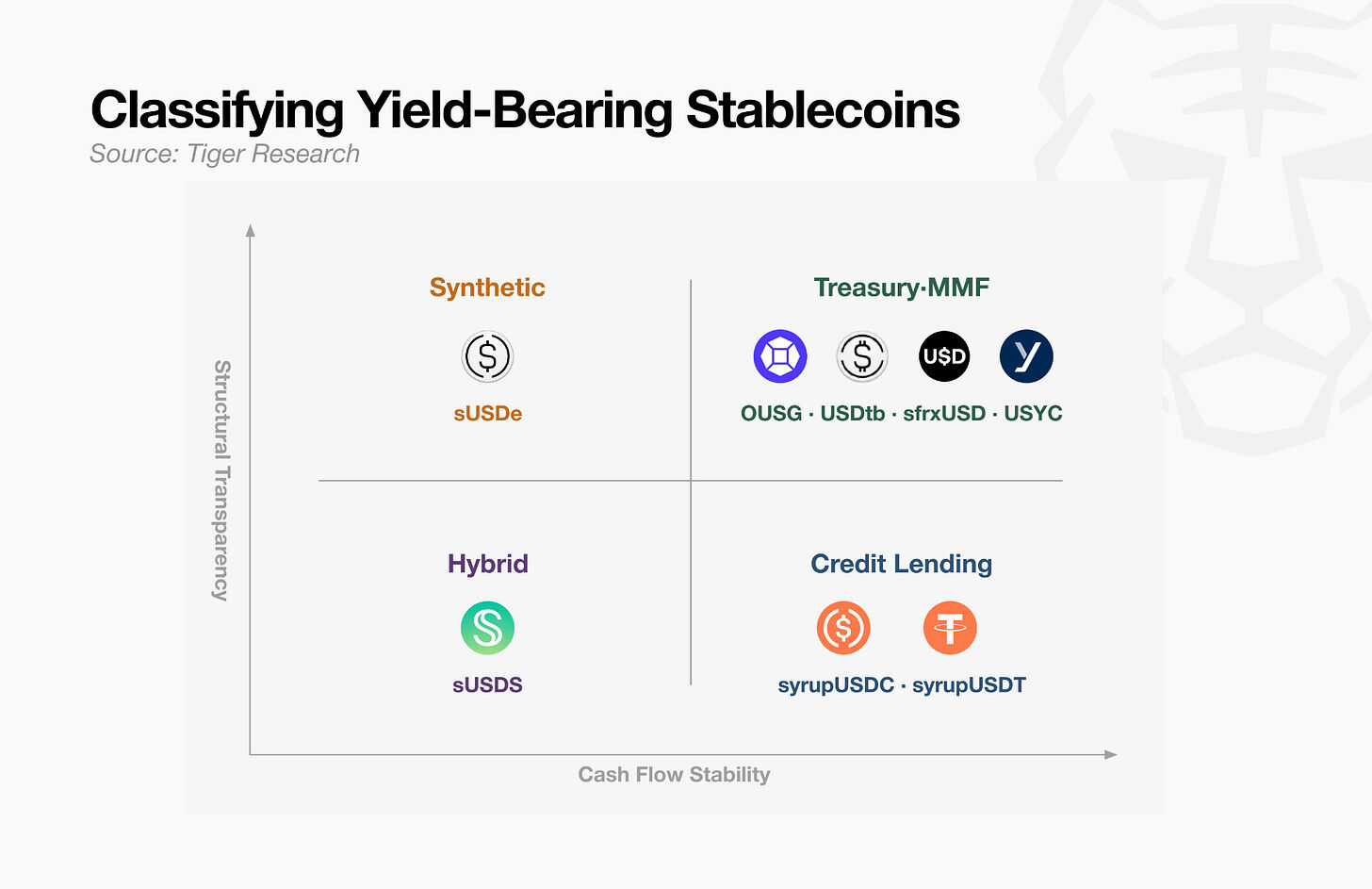

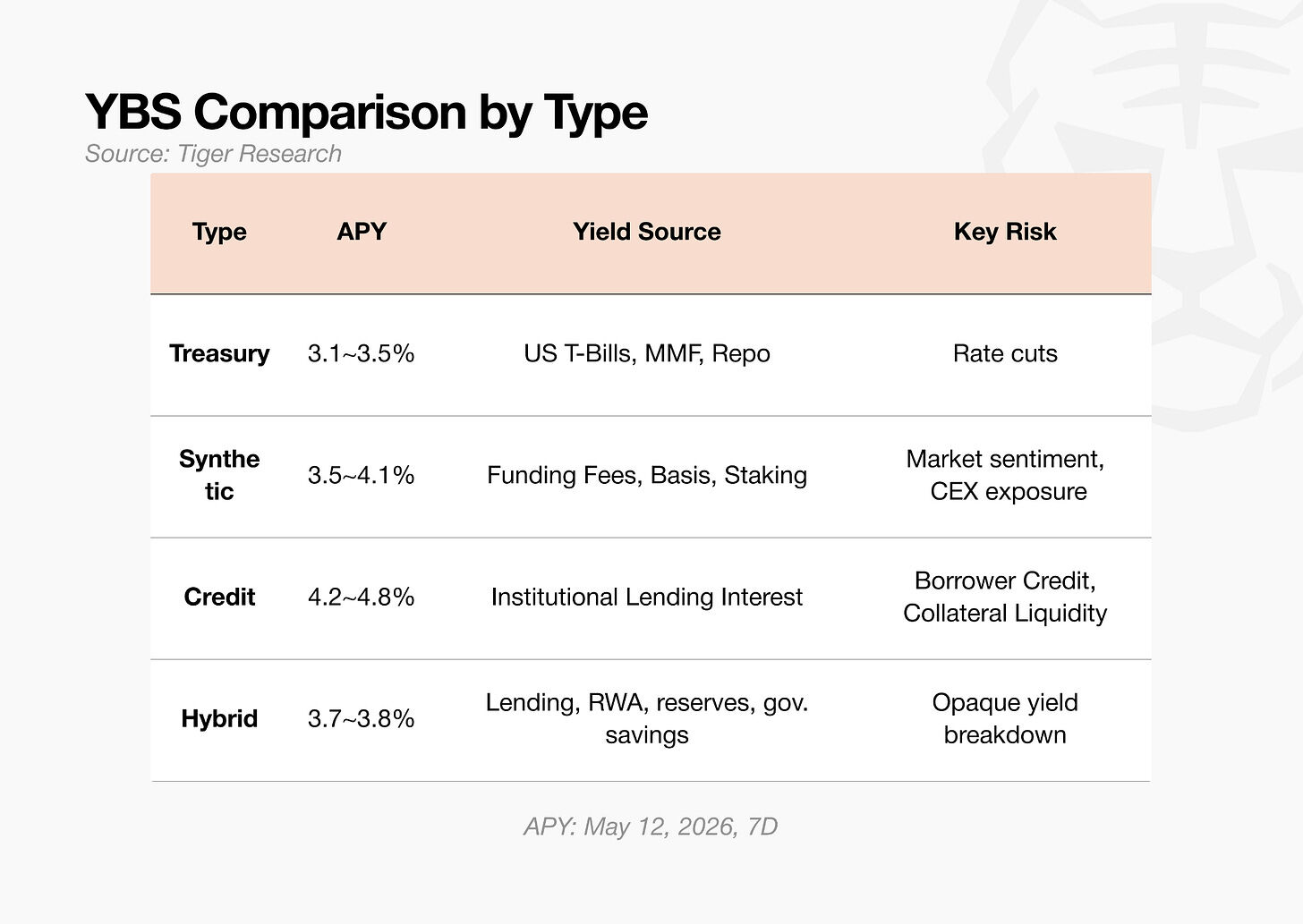

YBS MARKET DIRECTION

YBS ASSETS ARE CLASSIFIED ALONG TWO AXES: "HOW STABLE THE RATE OF RETURN" AND "CAN THE SOURCE OF THE PROCEEDS BE VALIDATED"? 4% OF APY IS NOT ALWAYS THE SAME 4%. THE TYPE OF RISK DEPENDS ON WHO IS PAYING INTEREST. MOST OF THE FUNDS ARE MOVING TOWARDS A MORE PREDICTABLE SIDE。

National debt support for YBS (OUSG, sfrxUSD, USYC) is the easiest to describe。

THE RATE OF RETURN ON SHORT-TERM NATIONAL DEBT FLOWS FROM THE ISSUER TO THE HOLDER THROUGH THE OPERATING LAYER. AS OF MAY 2026, THE AVERAGE APY WAS BETWEEN 3.1% AND 3.5%. THE CONSTRAINT IS THAT THE RATE OF RETURN IS TIED TO THE RATE OF INTEREST ON THE NATIONAL DEBT。

Synthetic YBS (sUSDe) provides transparent sources of income but is sensitive to market conditions。

THE MAIN SOURCE OF REVENUE IS THE FUNDS FOR THE CONTINUATION OF CONTRACTS. THE RATE OF RETURN CAN BE TESTED ON THE CHAIN BUT FLUCTUATES SHARPLY WITH MARKET CONDITIONS. ASY EXCEEDED 15% IN SEPTEMBER 2025 AND THE 7-DAY BENCHMARK AS OF 12 MAY 2026 WAS IN 4% RANGE。

The credit class YBS (syrupUSDC, syrupUSDT) has a high rate of return that is stable but less verifiable。

Through Maple Finance, interest paid by hedge funds and trading companies flowed back to the holder. The fixed interest rate structure remained low at 4 per cent. The credit and collateral value of borrowers is difficult to check externally。

Mixed YBS(sUSDS) is between two ends。

The rate of return is mixed with Spark borrowing costs, RWA returns, reserve management and the savings rate set by governance. 7 Days interest rate 3.6 per cent, lower than sUSDE. On the risk side, a lack of single point failure would help. The trade-off is difficult to structure from external parts of the proceeds。

This classification points to a single model: With the exception of Ethena's synthetic model, each category is moving the sources of traditional financial gains into chains。

Ethena knew

Ethena's first signal of recognition of its own structural constraints is the introduction of USDtb. USDtb is a US dollar-backed national debt, with short-term United States Treasury debt as a reserve. It is designed to provide a buffer for USDE at the time of the transfer of financial rates。

In April 2026, Ethena took further action to directly transform the collateral structure of USDe. Ethena reduced its share of the sustainable contract to 11 per cent of the total collateral and added new categories: stable currency reserves, DeFi lending, CLO, investment-grade corporate bond funds, short-term credit。

Ethena is also working on plans to include a delta neutral strategy based on a gold lasting contract in USDe collateral. The structure will be used for the same BTC and ETH methods for gold (PAXG, XAUT). The risk committee has completed its formal review。

This is the largest structural change since its launch. In fact, Ethena admits that the Delta neutral strategy, built solely on encrypted assets, is no longer valid。

USde and sUSde are evolving from synthesis to mixing. This shift recognizes that a single source of income is no longer sufficient to remain competitive in the YBS market。

Base priority

DeFi ' s revenue from traditional financial imports, rather than from origin, may run counter to the concept of decentralised finance. But that doesn't mean DeFi is finished。

The block chain, which seeks to establish a decentrized Internet, ultimately operates on the Internet itself. There are no block chains without the Internet. The stabilization currency, which was intended to replace the dollar, eventually operated above it. They then contributed to the rise of DeFi. The traditional foundations have never prevented innovation from the top。

YBS can go the same way. BuIDL is already a USDtb collateral. USDtb became a reserve for USDm. The new currency Lego has stacked over the national debt support YBS。

As the national debt supports YBS sank into infrastructure, the rate of return is reduced and the range of assets at the bottom is narrowed. The alpha available for any single asset will continue to shrink. Just as the Internet becomes infrastructure and access costs are approaching zero, YBS will follow the same path. Stability and portability are more important than rates of return。

When the infrastructure is mature, the experiment to build it can operate on a stronger base. The early synthesis of the United States dollar was unsustainable because of the instability of its bottom assets。

Early DeFi revenue structure built on sand. They depend on the price of the banknotes, the incentives of the coins and the demand for leverage. The proven source of proceeds is now forming the foundation, and the chain financial architecture is building on it。